http://www.artmarketmonitor.com/2015/07/30/if-contemporary-art-is-so-great-why-doesnt-anyone-make-any-money/ If Contemporary Art Is So

Great, Why Doesn’t Anyone Make Any Money?

by

Marion Maneker

James Tarmy digs into Magnus Resch’s startling

look at the economics of running an art gallery. The result

isn’t pretty. After reading the book, Tarmy says, “It turns out

that the upbeat world of biennials and art fairs and parties is

in fact a cutthroat, antiquated, deeply flawed industry hampered

by an obsession with keeping up appearances and an often

misguided aversion to making money.”

Here are some more of the

startling things Tarmy discovered in Rensch’s book:

Fifty-five percent of the

galleries in Resch’s survey stated that their revenue was

less than $200,000 per year; 30 percent of the respondents

actually lost money; and the average profit margin of

galleries surveyed was just 6.5 percent.

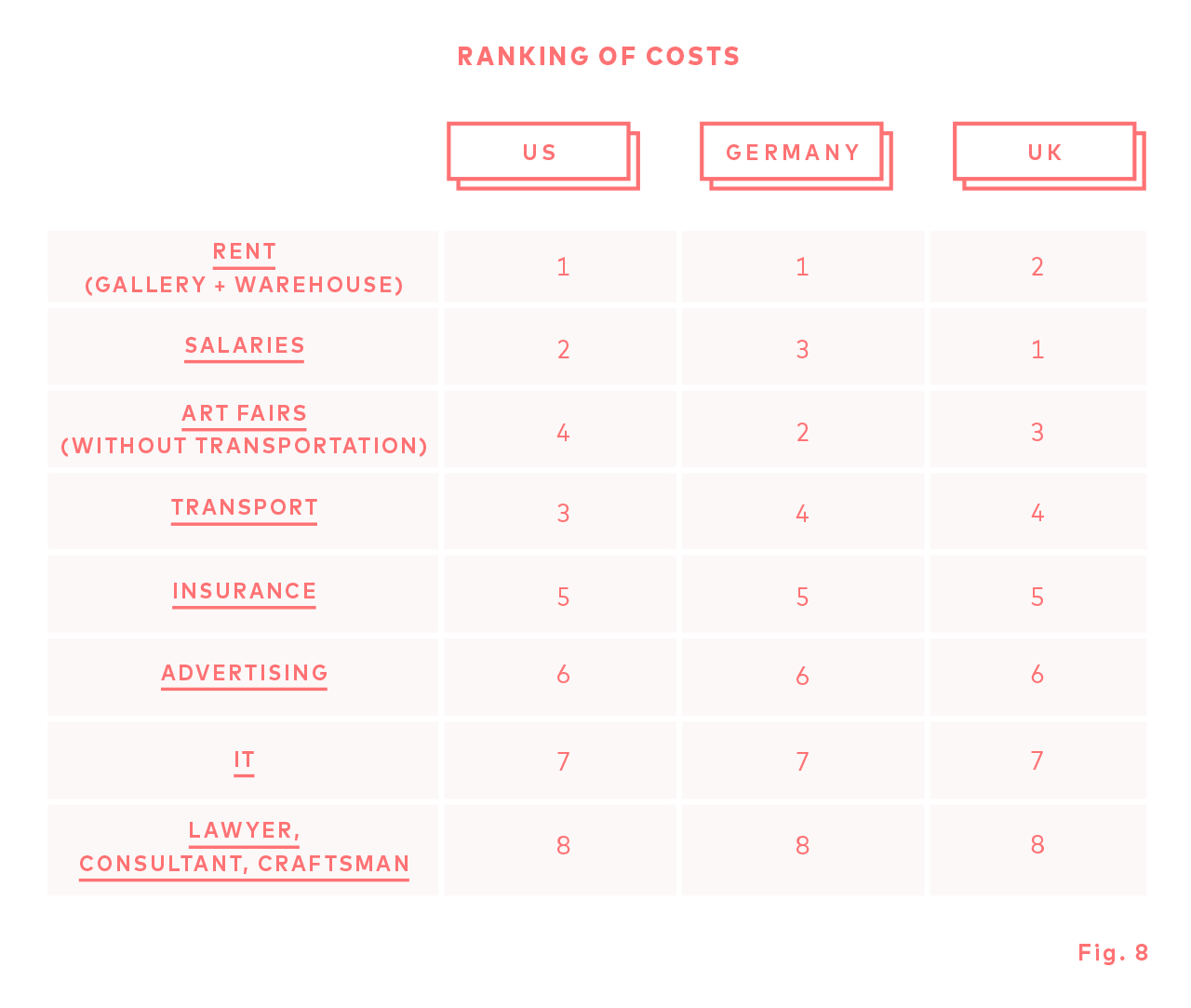

In the U.S. and Germany, the

physical cost of an exhibition space was listed as

galleries’ greatest expense (in the U.K. it was second),

and Resch writes that “the almost unanimous, and

unquestioned, conviction that central premises in a major

city are essential simply cannot be justified with an

economic rationale.” In other words, collectors will go

wherever the art is, and everyone else—the inevitable crowds

at openings, the passersby who pop in to see whatever’s on

view—has no bearing on the gallery’s bottom line.

Galleries generally split the

sale of a work 50/50 with the artist. Resch argues

that—given that galleries often have to cover marketing,

production, shipping, and insurance costs—it should be

closer to 70/30. Cue artist outrage.

http://www.bloomberg.com/news/articles/2015-07-30/why-do-so-many-art-galleries-lose-money- Why Do So Many Art Galleries Lose

Money?

The art business is booming, but

many galleries are barely getting by. One German expert thinks he knows

the answers

by James Tarmy, July 30,

2015 — 10:38 PM BST

The exterior of

New York’s Wallspace gallery, which announced it

would close next month. Source: Object

Studies, New York via Bloomberg

On Tuesday, the highly respected

Wallspace gallery in Manhattan’s Chelsea neighborhood

announced it would close its doors permanently on Aug. 7.

The lease was up, and “it necessitated a reevaluation,”

said Jane Hait, who co-founded the space with Janine Foeller.

“It’s a particularly tough climate for people doing work

that’s not necessarily super commercial.” The closure of

such a celebrated fixture of the New York art

scene underscores the fact that—despite the

unprecedented avalanche of money blanketing the

contemporary art world—it’s surprisingly difficult for

galleries to make money.

The news of Wallspace’s closing comes just weeks

before the English release of

Management of Art Galleries, a slim, Day-Glo orange

book that caused a

furore when it was published in Germany last year.

Written by a 31-year-old German entrepreneur/professor/art

adviser named Magnus Resch, the book argues that most

galleries are undercapitalized and inefficient, and

moreover, that with McKinsey-like business strategies (Resch

went to the London School of Economics and the University of

St. Gallen, in Switzerland), the entire art market could be

turned into a profit-generating machine. “I could have just

said, ‘The revenue numbers are terrible,’ but rather than

being so negative I’m actually offering solutions,” Resch

says in an interview. “It’s based on the analysis that I

did.”

Magnus Resch, who authored the controversial

book Management of Art Galleries.

Source: Magnus Resch via Bloomberg

Under different circumstances, Resch’s claims would probably

have been waved away, but in what’s close to a first for the

gallery world, he has the data to back them up.

Last year, Resch sent out an anonymous electronic survey

to 8,000 galleries, and more than 16 percent, or about 1,300

people, responded with information about their revenue,

number of employees, and location. (The original version of

the book included data for just Germany. The English

translation includes data for the U.S., the U.K., and

Germany.)

The results are grim: Fifty-five percent of the galleries

in Resch’s survey stated that their revenue was less

than $200,000 per year; 30 percent of the respondents

actually lost money; and the average profit margin of

galleries surveyed was just 6.5 percent. (Lest a critic

argue that the pool was too skewed to rural galleries

selling crafts, or decorative arts galleries buckling under

the weight of their unsalable Louis XV chairs, 93 percent of

Resch’s respondents represent contemporary art galleries.)

After laying out his data and methodology, Resch

isolates what he considers galleries’ key impediments to

profitability.

The Rent Is Too

High In the U.S. and

Germany, the physical cost of an exhibition space was listed as

galleries’ greatest expense (in the U.K. it was second), and Resch

writes that “the almost unanimous, and unquestioned, conviction

that central premises in a major city are essential simply

cannot be justified with an economic rationale.” In other words,

collectors will go wherever the art is, and everyone else—the

inevitable crowds at openings, the passersby who pop in to see

whatever’s on view—has no bearing on the gallery’s bottom line.

Paying a premium for a desirable location, according to Resch,

is therefore pointless.

Artists Make Too

Much Galleries

generally split the sale of a work 50/50 with the artist. Resch

argues that—given that galleries often have to cover marketing,

production, shipping, and insurance costs—it should be closer to

70/30. Cue artist outrage.

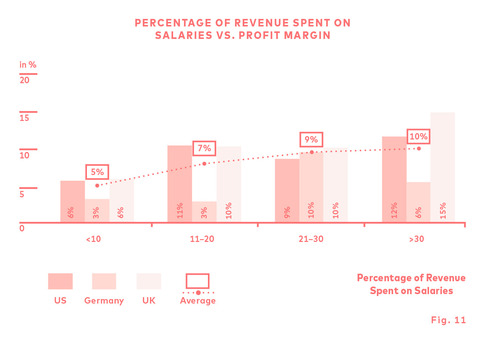

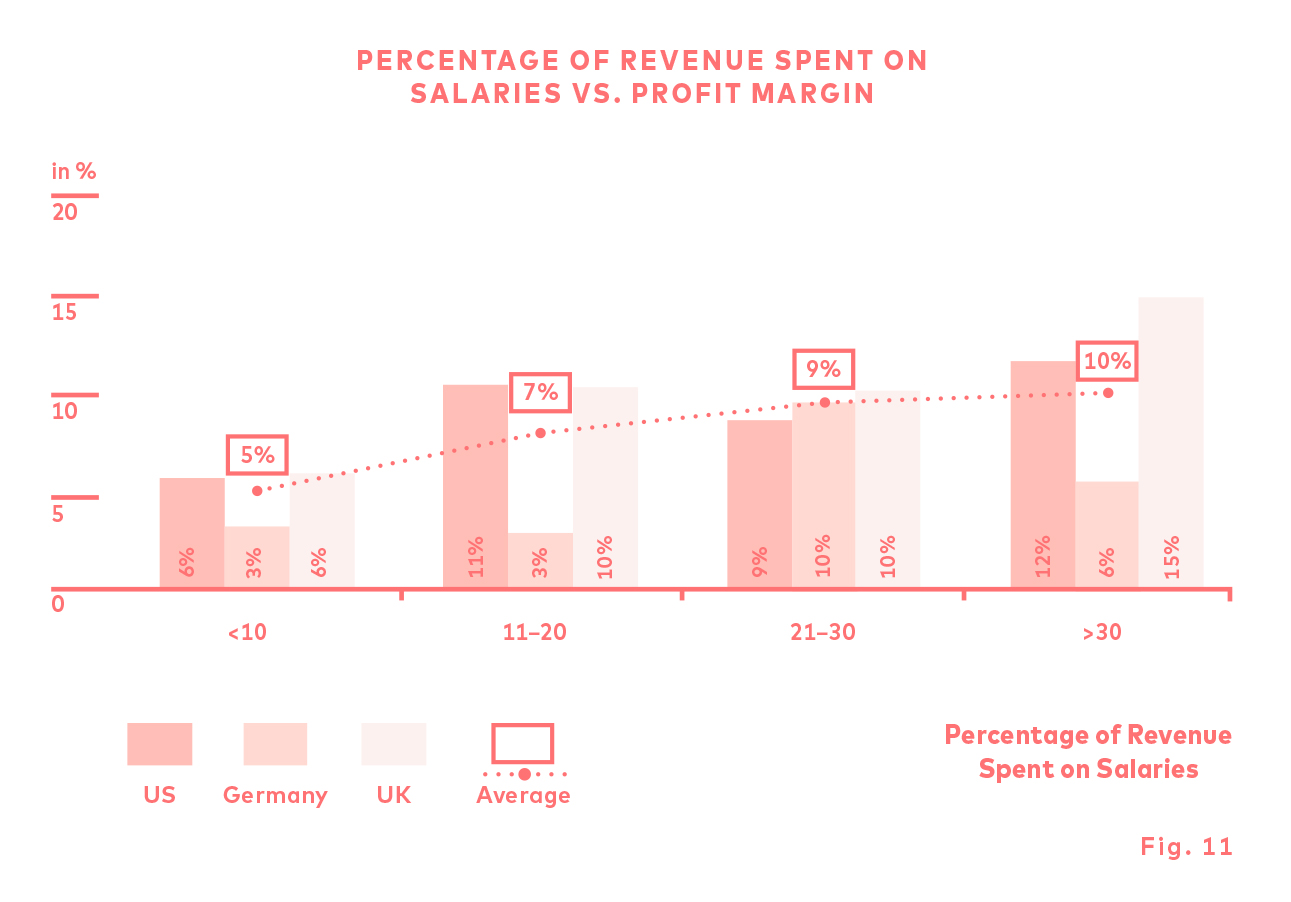

Gallery Staff

Make Too Little This is an

interesting one. Resch discovered that the more a gallery spent

on employee salaries (percentage of revenue allocated to

employee salaries vs. profit margin), the more profitable the

gallery became. In one respect, this makes intuitive sense: Once

a gallery is successful, it can afford to pay its employees

more. But Resch says that higher pay, tied to performance, is a

greater incentive—the more money employees make by doing well,

the more they want to succeed.

Everyone Is

Selling the Same Thing Resch

points out that the vast majority of galleries were competing

for the same, tiny world of contemporary art collectors.

Diversify, he suggests. This is easier said than done, though:

Sure, the contemporary collector base is small—but the

group interested in other periods (11th century illustrated

manuscripts, say) is even smaller. That’s basically why everyone

is selling variations of the same art; it’s simply what

collectors want to buy.

Resch has other points—galleries

are terrible at marketing and branding; they’ve done a horrible

job of expanding their collector base; they’re not active enough

in the secondary market; they fail to innovate their business

models in any measurable way—but those are less connected to the

data and more closely aligned with Resch’s background in

business. His recommendations (he’s careful not to call them

solutions) range from the reasonable (galleries should have

rigorous contracts with their artists) to the jaw-droppingly

silly. In an effort to spice up the sales experience, for

example, he suggests that galleries use sparklers to denote sold

works at openings, and he makes the bold and perhaps

unintentionally self-deprecating statement that, due to the art

world’s low salaries, “the best educated people … will almost

always choose another industry to work in.” Ouch.

The realities of the primary art

market depicted by Resch’s data, however, are harder to argue

with. It turns out that the upbeat world of biennials and art

fairs and parties is in fact a cutthroat, antiquated, deeply

flawed industry hampered by an obsession with keeping up

appearances and an often misguided aversion to making money. No

wonder a gallery like Wallspace was forced to close. “Our

primary focus didn’t always correlate with financial success,”

according to Hait. “It’s unfortunate, because galleries doing

things like we were trying to do have a tough time staying in

business.”

http://en.artmediaagency.com/112875/do-art-galleries-need-to-review-their-business-model/ Do art galleries need

to review their business model? Berlin | 6

August 2015 | AMA

Magnus Resch’s book, Management

of Art Galleries, has just been published in Great Britain.

The book is based on a survey that was conducted of 8,000

galleries (with 1,300 respondents) in order to present a

study of the art galleries based in Germany, the United States

and Great Britain. The questions asked in the form covered the

galleries’ revenue, their localisation and their employees. The

author considers that galleries adopt particular strategies to

improve their profits, making them more competitive on the

market. In an article published on Artnet, he explains that the

first initiative to be taken should be “love the market and

start talking about money”. The book has stirred up controversy,

especially in terms of its angle, which was deemed rather

simplistic by a number of specialists. Art Media Agency decided

to go over the book’s key points in order to better grasp its

scope.

The work starts off with the

following question: “why are galleries losing so much money when

the art business is booming?” This observation can be supported

by a number of prestigious galleries who were forced to shut

down: Galerie Kamm, based in Berlin, closed its doors in 2004,

and the New York gallery Wallspace will put an end to its

business on 7 August 2015. The survey conducted by Magnus Resch

himself is bringing to light the economic difficulties that

galleries are facing: 55% of these galleries have stated that

their revenue was less than $200,000 per year and 30% of the

respondents are actually losing money each year. The average

profit margin of these galleries is 6.5%.

It’s true that these numbers

affirm that galleries are not all a surplus to the needs, but

it’s important to nuance this statement: the surveyed galleries

are far from homogeneous and some selection bias should be

brought to light. Not all participants in the survey are the

same size, which has an impact on their total revenue. Moreover,

the survey covers three countries in which the art market

differs: in an article he wrote for Artnet, Resch points out

that the German art market is more reluctant to talk about

economic profit, which is not the case in Anglo-Saxon countries.

Following the assessment of a low

economic profitability, Resch suggests a number of

recommendations, which he has formulated from his observations.

By studying the expenses of the galleries, Resch listed the

rent as one of the highest expenses (first in the United States

and in Germany. According to him, central premises in a major

city cannot be justified with an economic rationale: it’s the

offered objects that should attract potential buyers and not the

location of the gallery.

The second element Resch proposes

is to review the revenue sharing between the galleries and the

artists they represent. The majority of them operate on the

50/50 principle: artist and gallery equitably share revenue from

sales. Magnus Resch believes that the galleries bear significant

costs such as promotion, production and the costs associated

with insuring the works. Consequently, revenue sharing must be

returned to the galleries to make them more profitable. As such,

the split of the sale should be the gallery receiving 70% of

revenues, leaving 30% to artists. This point in particular is

quite controversial because the remuneration of artists’ work is

fundamental.

The survey also demonstrates that

there is a correlation between the galleries’ employees’ salary

and its revenue. According to Resch, a higher salary attracts

better qualified people and improves the profitability of the

gallery. In his article “Why Do So Many Art Galleries Lose

Money?”, James Tarmy emphasises that the link between the two is

not that obvious: it’s more likely that because the galleries

are profitable they can pay their employees higher salaries.

Finally, Resch focuses on the

structure of the galleries’ business: the majority of the

galleries (93 %) are specialised in contemporary art. Resch points

out that there are too many contemporary art galleries compared

to the number of buyers. He suggests that it would be smarter to

turn to other less competitive segments of the art market.

However, James Tarmy explains that contemporary art is in high

demand, and if there are that many galleries specialised in that

sector, it’s to meet the demand. Specialising in a different

sector would thus not increase the volume of sales nor the

profitability of galleries.

Resch is an entrepreneur of

German origin, specialised in art. He founded an art gallery at

the age of 20 and currently works as a Management of Art

professor at the University of St. Gallen in Switzerland.